Spare The Rod, And Spoil The Chaebol

Noah Smith says that he has long been an industrial policy enthusiast in his latest post. Like me, he too is a fan of Joe Studwell’s excellent book, How Asia Works. You should read his many excellent posts on this topic, including the one I linked to at the start of this post.

In that post, he makes three main points:

For developing nations, attracting FDI is as good a form of industrial policy as any

For developed nations, technology policy is industrial policy today

And China’s approach is riddled with risks

I’m mostly in agreement with all of these points, though with a topic as complex as industrial policy, there will always be nuances. But in my post, I want to talk about one of the sections in his post. It is titled thus: “Industrial policy” has become too broad of a category. It is this discussion that allows him to segue into what type of industrial policy is best for which type of nations, leading to the three points I referred to above.

But regardless of how you define industrial policy (and my own definition can be found below), I think there ought to be one definitive ingredient that makes or breaks this dish, and that ingredient is often missing in many different versions - especially the modern day ones. That one ingredient is negative incentives.

Incentivizing someone to do something by giving them a reward for it is a positive incentive. But one can also ensure that the task is done by threatening to punish them if it is not done. That is an example of a negative incentive.

In what follows, I will make the following arguments:

Industrial policy is much more likely to fail because negative incentives are missing

These are hard to design, and even harder to enforce

Culture is an underrated reason for this, and that is a major problem for industrial policies the world over.

But let us begin by trying to understand what industrial policy is.

What is Industrial Policy?

Noah defines it in his post: government promotion of specific industries. We do not let market processes play out, in other words. The government does not just regulate a particular sector, but participates in it, at least indirectly. It does so by, in effect, tilting the playing field. Some players get an undue advantage, for at least a specified period of time. These players are almost always domestic players, rather than foreign ones, and the idea is to have those domestic firms get better over time.

How long a period of time? On what basis? Which players, and how are they to be chosen? What exactly does the absence of a level playing field mean? How does the government enforce this, and do other players (both domestic and foreign) not protest? How are these supports monitored, and when and how should they be taken away? The answers to all of these questions are the nuts and bolts of industrial policy, but you should be able to see that all of these questions are downstream of Noah’s pithy definition: industrial policy is the government’s promotion of specific industries.

Even the most laissez-faire of economists will accept the need for industrial policy when push comes to shove. We may debate, for instance, about what the correct industrial policy ought to be for AI in India, and as with all such debates, we may never end up with a definitive answer. But there is unlikely to be much of a debate about the proposition that Indian firms can compete at the very cutting edge of the AI sector absent government support. That leads us to an interesting, and somewhat mischievous proposition - the debate isn’t really about whether industrial policy is good or bad. It is about the circumstances in which such policies are warranted.

And today’s facts are such, sir, that everyone has changed their mind.

Industrial Policy is Hard, And This is Why

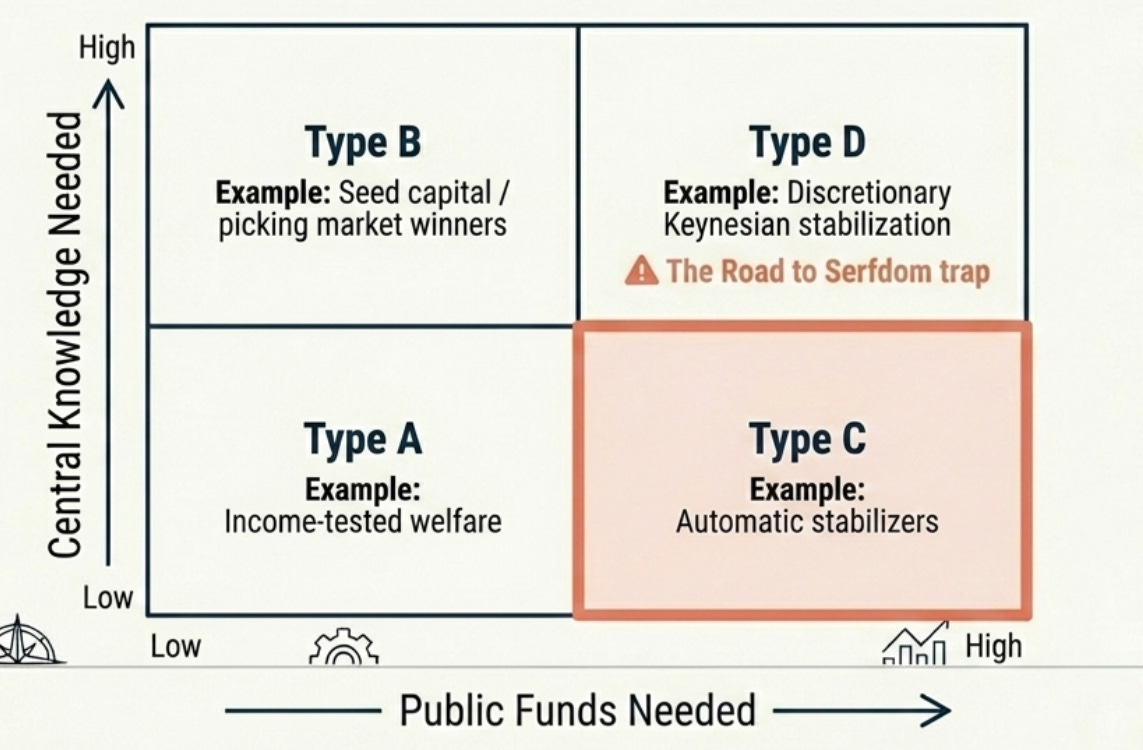

Critiques of industrial policy are not just warranted, but they are almost always going to be right. And this is so because industrial policy comes up against perhaps the hardest problem in all of economics: the knowledge problem. The infographic above is from a presentation that NotebookLM made for this paper, and it makes a devastating point. Industrial policy sits at the top left corner, and this corner has good news and bad news. The good news is that while the absolute amount of funds needed for industrial policy may seem large, they are usually a small percentage of the total public funds available at the disposal of the government. Certainly smaller, as the infographic shows you, than Keynesian stabilization policies.

But the bad news is that such policies require central planners (the government) to have a very high level of knowledge. It is one thing to say “pick market winners” and quite another to answer the question “on what basis?”. Answering that question necessarily implies having a lot of knowledge about not just the sector, but also about each individual firm. Worse, much of that knowledge is tacit knowledge. It is not a line entry in a report, or a number in a balance sheet. It is often about hiring decisions, or about culture, or about know-how - and perhaps most devastating of all, it is dynamic. What is true today may not be true tomorrow - a key employee may leave, culture may evolve, technologies may change - and all of these things happen all the time in all firms. Anybody who has worked in one will know this to be true. So for any one entity to have all of this knowledge and for it to be up to date… well, that is, to quote from economic scripture, a problem.

IP Needs To Cut Both Ways

Joe Studwell’s book has this powerful anecdote:

It was twelve days after the 1961 coup, on 28 May, that Park and his colleagues began arresting businessmen. They did so under a Special Measure for the Control of Illicit Profiteering. There are conflicting accounts of how many businessmen were held, where and for how long. But it is clear that scores of the country’s most senior entrepreneurs were locked up. Seodaemun was one detention point. A few top figures, including Samsung’s founder, Lee Byung Chull, had the good fortune – or, more likely, the forewarning – to be in Japan. But the great majority of the country’s business elite was taken in. Park put the frighteners on the business community in a manner unprecedented in a capitalist developing country. He declared that the days of what he termed ‘liberation aristocrats’ – crony capitalists who bought favours from Syngman Rhee’s government and did nothing for their country in return – were over.

Imprisoned businessmen were required to sign agreements which stated: ‘I will donate all my property when the government requires it for national construction.’ In effect, this put the entrepreneurs on parole to do whatever Park required. The most senior group, including Lee Byung Chull after he returned from Japan, quickly agreed to pursue investments in industries – mostly manufacturing ones – that the military and a handful of bureaucrats familiar with Japanese industrialisation wanted to develop: fertiliser, synthetic fibres, cement, iron and steel, electricity generation, and so on. They formed the Promotional Committee for Economic Reconstruction (PCER), later to become the Federation of Korean Businessmen, as the formal channel through which big business communicated with the government and aligned itself with state objectives. Samsung’s Lee was the first chairman. The leading business families also agreed to the renationalisation of banks which had been privatised to them, under US pressure, in 1957. The banks had become a destabilising source of illegal lending to their owners’ firms, a problem that has afflicted privatised banking systems in developing states from Meiji Japan to post-Second World War south-east Asia and Latin America.

Once he established the basic rules of the game, Park informed Korea’s businessmen that they were free to make as much money as they could so long as they stuck by the rules.

The reason I call it powerful is because it doesn’t conform to received wisdom about industrial policy. This isn’t about providing support to sectors, firms or industries. Quite the opposite, in fact, and in a rather hair-raising way. The state demonstrated its willingness to do scary, hard and downright brutal things first. It then stated its own demands, and indicated a willingness to do what it took to enforce them. And once it established the rules of the game, it made clear to the businessmen that they were ‘free to make as much money as they could’... so long as they stuck by the rules.

I am not suggesting that any country lock up its businessmen today. Nor am I suggesting that such measures are the only way to make industrial policy work. But what I am suggesting - and very strongly - is that we need negative incentives for industrial policy to work. That infographic in the previous section explains why it is all but inevitable that governments will end up picking, at least in some cases, the ‘wrong’ winners. That, given Hayek’s insight, is an inevitability.

The countries that succeeded in industrial policy had this problem, as did the countries that failed. The difference is that the successful countries got out of this problem fairly quickly. And they did so by using negative incentives. To quote Studwell in the case of those countries where IP worked, ‘the state did not so much pick winners as weed out losers’.

And again, that graph helps us understand that picking winners is a fool’s errand. Hayek told us long ago that it couldn’t be done. But weeding out the losers could be done. In Japan, for example, Studwell tells us that ‘the amount of depreciation that firms were allowed to charge to their accounts was determined by their exports. In Korea, firms had to report export performance to the government on a monthly basis, and the numbers determined their access to bank credit.’

IP is about the carrot, but don’t forget about the stick.

Easier Said Than Done, Alas

Back in December 2025, Richard Hanania wrote a post with the title Human Capital, Not “Industrial Policy”, Explains East Asian Success. The post argues against the thesis advanced by Studwell, and says that the success of East Asia is explained much better by culture/genetics, rather than by policies. Not that policies aren’t important, he says, but they are secondary to culture/genetics. The use of the word ‘genetics’ will raise many hackles, he says, so he restricts himself to talking only about culture - and we’ll follow suit in this section. But do keep in mind when you read this section that he means both of these things.

And one of his biggest arguments against Studwell’s thesis is that Studwell constantly and consistently underrates culture:

“Studwell’s refusal to consider any kind of human capital or culturally based explanations leads him into some entertaining directions. I got a particular kick out of this part:

“In this respect, land policy is the acid test of the government of a poor country. It measures the extent to which leaders are in touch with the bulk of their population – farmers – and the extent to which they are willing to shake up society to produce positive developmental outcomes. In short, land policy tells you how much the leaders know and care about their populations. On both counts, north-east Asian leaders scored far better than south-east Asian ones, and this goes a long way to explaining why their countries are richer.”

So Northeast Asian leaders just cared more about their people? What kind of explanation is that? Maybe it’s a cultural thing? But the whole book is about cultural explanations not having any power, and the need for us to focus exclusively on policy. So I guess Studwell’s theory is leaders who care → the right industrial policy → economic development. But I think once you’re adopting theories based on the idea that some governments are just staffed by better people, you’re conceding a lot to cultural theories, which is odd when your entire thesis is that they need to be rejected”

The academic in me is inclined to agree with this point, and with the start of his concluding section:

“Capitalism works. With the collapse of the Soviet Union, and more recently the US surpassing Europe, East Asia stands out as the one region of the world that supposedly shows that government planning can be beneficial as long as it does not go overboard.

I see no reason to grant this argument. Countries succeed or fail based on a combination of population traits and policy. When we hold cognitive ability as measured by PISA constant, we see that more free market jurisdictions do better than the alternative: the US outperforms Europe and East Asia, and among East Asians, Singapore and Macau are the two places that clearly overperform their potential given standardized test scores. In Europe too, the most free-market countries have grown the fastest in recent years.

One more thing to note here is that advocates of industrial policy are often even more irrational than indicated by the discussion above. Studwell was presenting his suggestions as a way for poor countries to get out of poverty and start developing. He wasn’t arguing for a set of prescriptions for first world countries to adopt, and explicitly says that the case for free capital markets becomes stronger the wealthier you get.”

The one thing that I would certainly say about this excerpt is that the world is more complex than any one cross-country regression can explain. There are always going to be more factors at play, and these are going to change over time. That is inevitable.

So What?

The synthesis that I’m trying to get at is that both Studwell and Hanania are right. As I said above, the academic in me is in agreement with most of what Hanania is saying here. But the Indian in me (I was born in 1982) cannot help but think about what we got wrong with our industrial policy in India, and what we might have done if Bhagwati and Manmohan Singh had ‘won’ their debates back in the 1960’s. Hanania would probably say that even that would have been wrong, and we should just have gone with opening everything up right away, and letting markets do their thing.

But the more I learn about our culture, our politics, our history and our policies, the more I realize this wouldn’t have been possible. Economics, as Amit Varma is fond of saying, is downstream of politics, and that matters from a policymaking perspective. It would be naive to think otherwise, especially for India back in the 1960’s.

So what is the synthesis that I am trying to get at?

That industrial policy did matter for East Asia back then (go Studwell!), and the reason it succeeded there, and not elsewhere is because of culture (go Hanania!). The reason it succeeded there was because it was one of the few places on earth that applied both the carrot and the stick - and applying the stick is only possible with very high state capacity. And very high state capacity is a function of… culture.

Neither culture nor industrial policy are guarantees of success, either individually or in tandem. There must be other factors at play, and I don’t pretend to have a secret recipe that any country at any stage of development can follow with a guarantee of success. And I certainly don’t mean to suggest that the culture of any country is an immutable thing that guarantees success or failure for all time to come. But I do say that industrial policy that encompasses negative incentives is likelier to work, and I also maintain that getting this to happen is heavily dependent on state capacity. That actually makes me a little more pessimistic about industrial policy working well in India!

As usual, I hope you disagree, and I look forward to you telling me why!

Great post. I don't see why it would have been naive to think of India pursuing some path other than brainless socialism in the 1960s. As I keep saying, no other civilization *worships* a goddess of wealth. Culturally, in my opinion, it's the most capitalist place on earth (a pundit took a call to negotiate a price on another funeral *while* conducting my mother's funeral, and no one thought it odd--business comes first). To me the real puzzle is why an entire country--historically open to the world and trading with everyone--would adopt idiotic Fabian Socialism and import substitution, seemingly born in the Harrow School in the 1920s.